Hey! It's Sarah Li

I’m a Product Designer in San Francisco. Currently leading developer tools at Twilio.

> I’m obsessed with solving problems and multiplying impact at scale, building great designer-developer relationships, and making products, teams, and systems that last.

Work

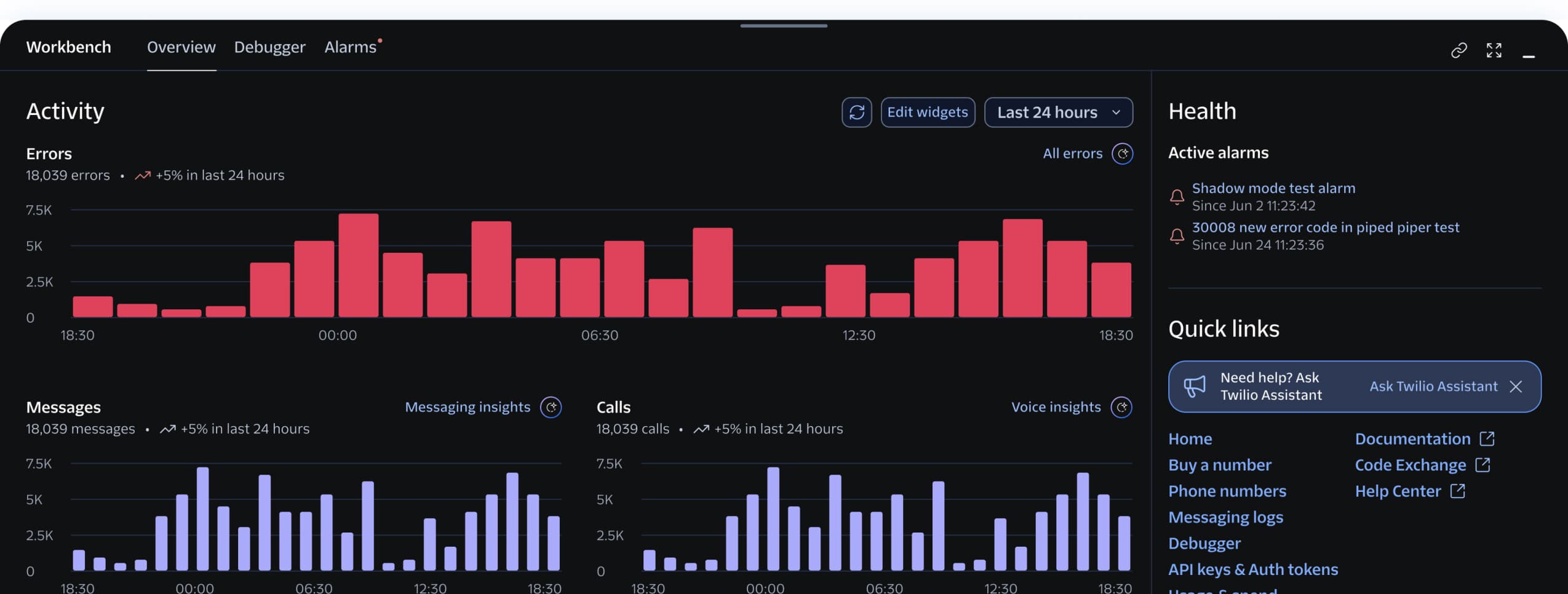

Twilio Workbench

I lead the design of Workbench, Twilio's platform-wide developer tools surface, enabling developers to troubleshoot and manage their integration across Twilio products without context-switching.

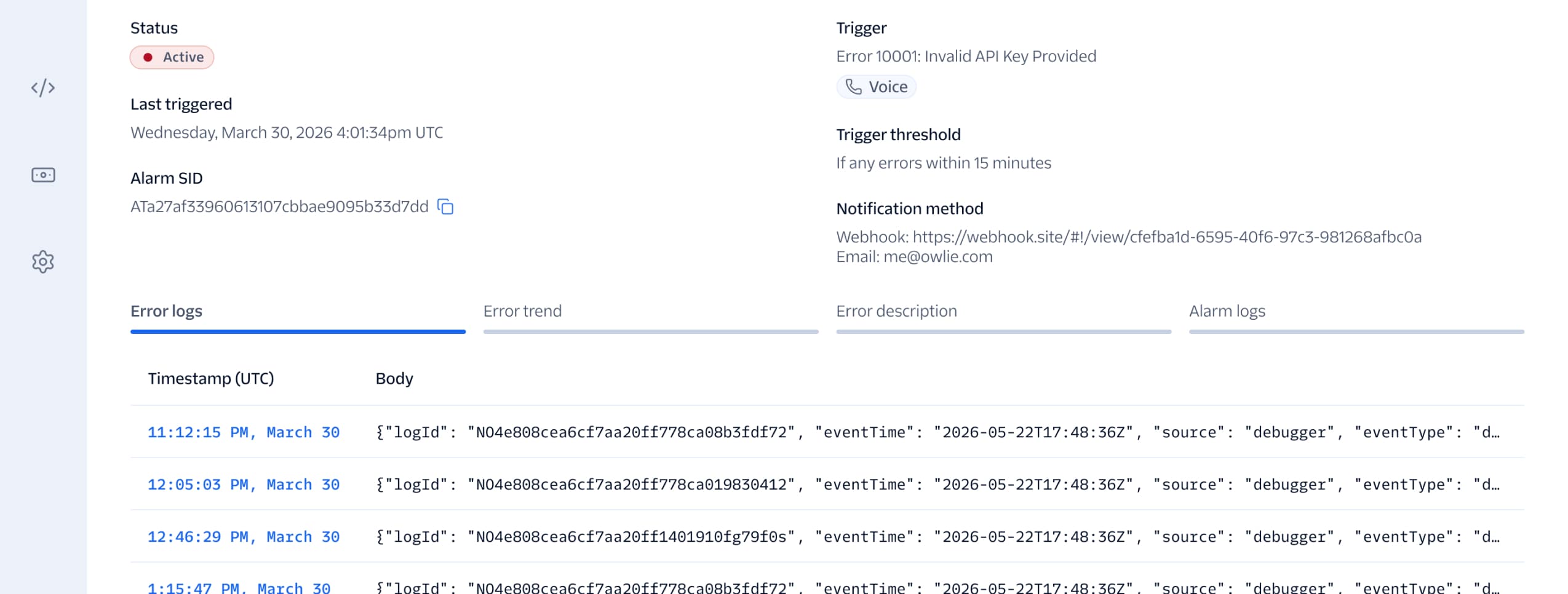

Developer tools and observability

I also lead the design of Twilio's additional developer tools and observability features, including AI agent observability, debugger, alerting, and webhook configuration.

Paste, Twilio's design system

I launched Twilio’s design system, led its 5-year evolution, and made some friends along the way. After starting from scratch in 2019, we drove adoption within all 30+ products at Twilio and undid over 10 years of front-end tech debt. I managed a design team that brought cohesion to the Twilio product suite, and unified the navigation experience across our 4 major product platforms.

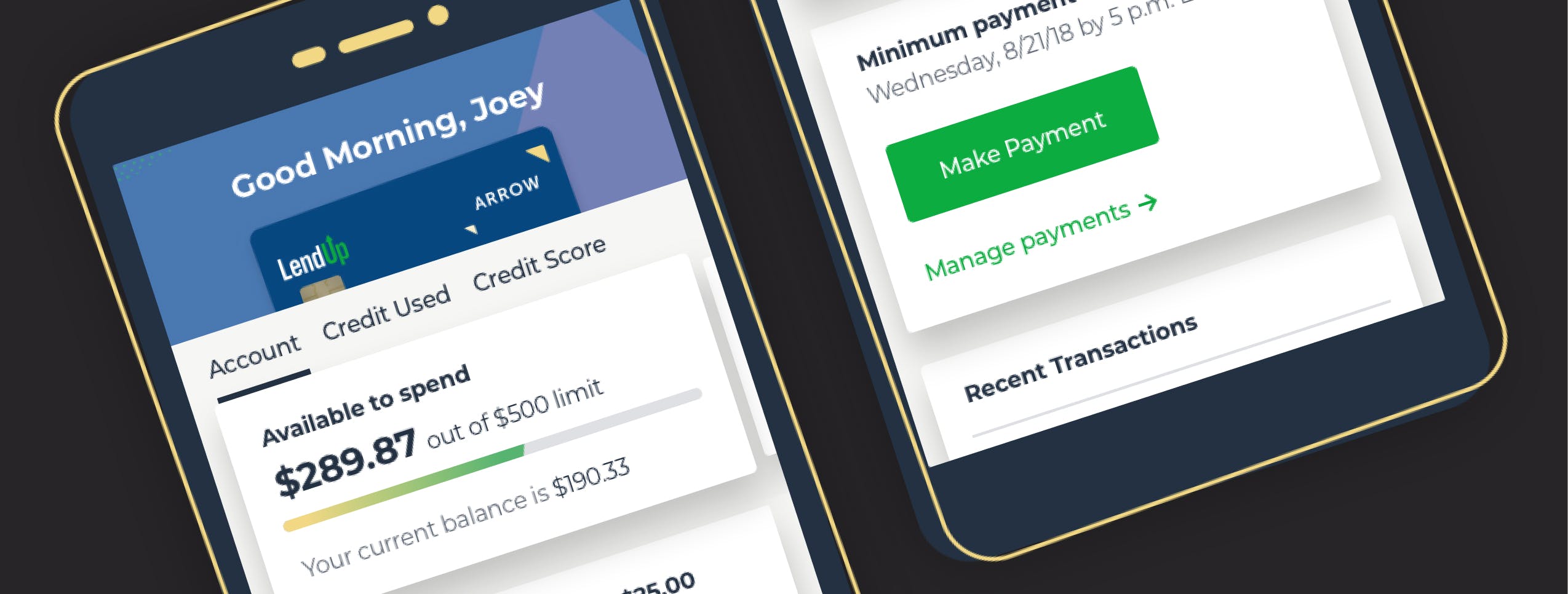

Arrow Card dashboard

At LendUp (now Mission Lane), I was on the launch team for the Arrow credit card app for iOS and Android. I designed account dashboards and payment experiences for 95,000 monthly active customers and decreased our support team’s call volume by 40%.

This website is a love letter to Paste and the beautiful humans I’ve had the joy and agony of building it with during some of the weirdest, toughest times on this earth.

@serifluous everywhere else