Hey! It's Sarah Li

I’m a Product Designer in San Francisco. Currently leading design systems at Twilio.

> I’m obsessed with solving problems and multiplying impact at scale, building great designer-developer relationships, and making products, teams, and systems that last.

Work

Paste, Twilio's design system

I launched Twilio’s design system, led its 5-year evolution, and made some friends along the way. After starting from scratch in 2019, we drove adoption within all 30+ products at Twilio and undid over 10 years of front-end tech debt. I managed a design team that brought cohesion to the Twilio product suite, and unified the navigation experience across our 4 major product platforms.

Coming soon

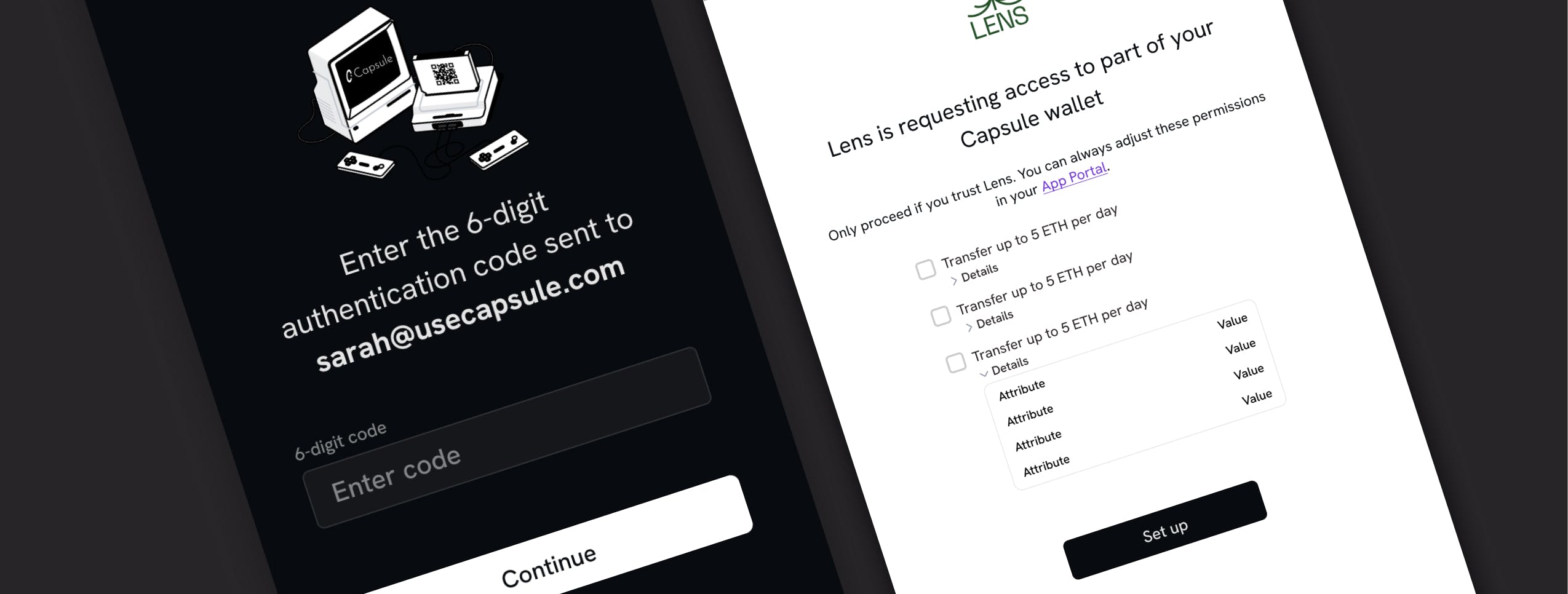

Twilio Artificial Intelligence UI Kit

Led the design of AI experiences across Twilio's Help Center and Console platforms, reimagining the future of our customers' experiences with AI and reducing support volume for our operations team.

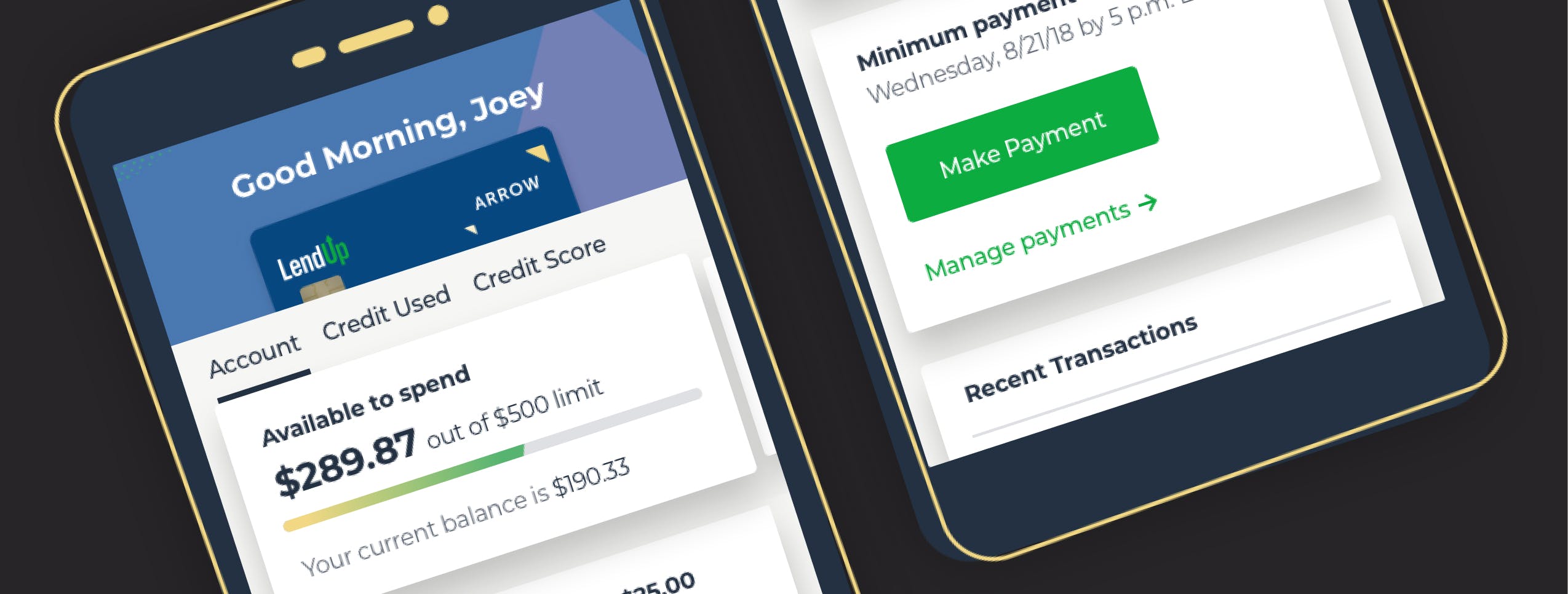

Arrow Card dashboard

At LendUp (now Mission Lane), I was on the launch team for the Arrow credit card app for iOS and Android. I designed account dashboards and payment experiences for 95,000 monthly active customers and decreased our support team’s call volume by 40%.

This website is a love letter to Paste and the beautiful humans I’ve had the joy and agony of building it with during some of the weirdest, toughest times on this earth.

@serifluous everywhere else